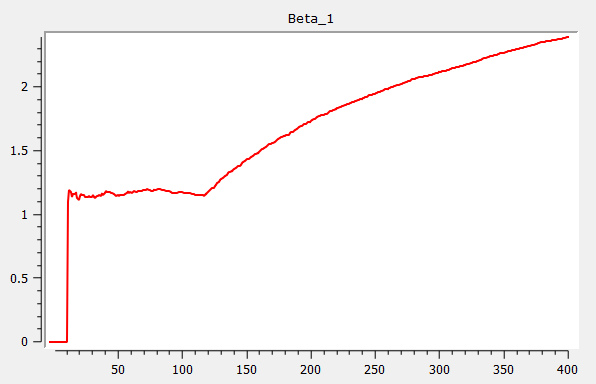

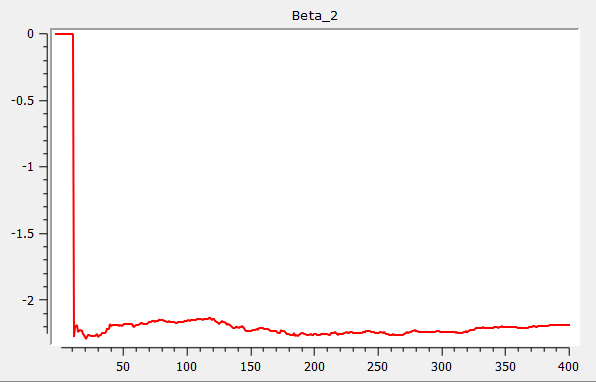

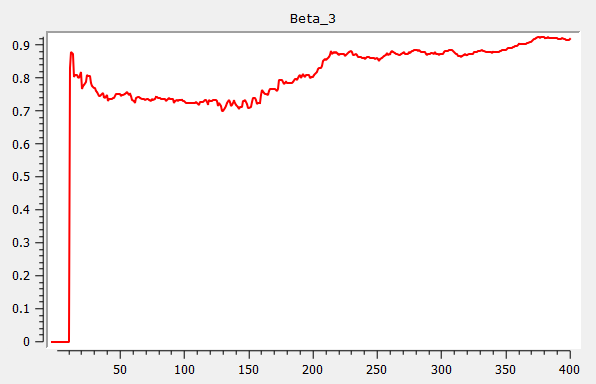

Example: Rolling estimation procedure

This example uses 400 observations of generated data with a break in the intercept after 120 observations. The error terms are standard normal. The data is replicated using the code below:

//Load TSMT library

library tsmt;

//Parameters for before (b1) and after (b2) break

b1 = { 1.2, -2, 0.75 };

b2 = { 5, -2, 0.75 };

//Number of observations before break

n1 = 120;

//Total number of observations

n_tot = 400;

//Simulate observations and error term

xt = ones(n_tot,1)~rndn(n_tot,2);

err = rndn(n_tot,1);

//Create series with break

y1 = xt[1:n1,.]*b1 + err[1:n1,.];

y2 = xt[n1+1:n_tot,.]*b2 + err[n1+1:n_tot,.];

yt_break = y1|y2;//Set-up expanding window size

wind = 15;

//Add specifies increment to increase window size by

//and is irrelevant for rolling window regression

add = 15;

//Gr is an indicator for graphing

gr = 1;

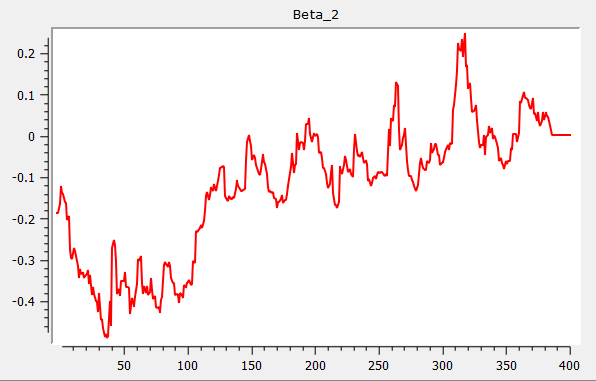

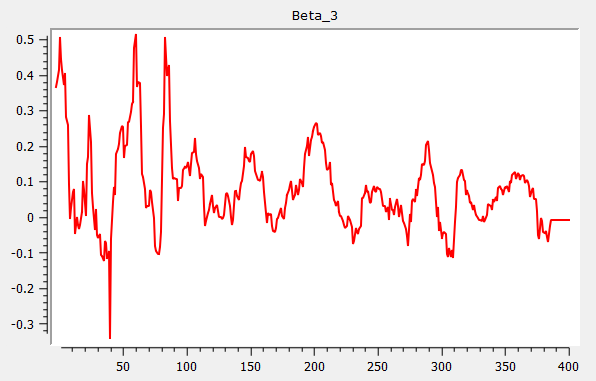

{ beta, res, w } = rolling(yt_break, xt, wind, add, gr);Which produces the following three graphs for Beta 1, Beta 2 and Beta 3:

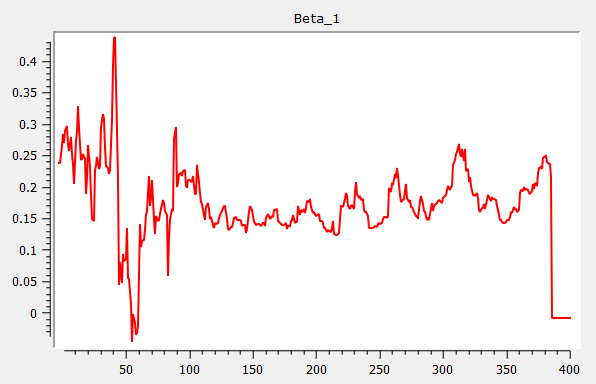

Finally we set parameters to run a forward expanding window regression and run the regression.

//Set-up expanding window size

wind = -15;

//Add specifies increment to increase window size by

//and is irrelevant for rolling window regression

add = 15;

//Gr is an indicator for graphing

gr = 1;

{ beta_fwd, res_fwd, w_fwd } = rolling(yt_break, xt, wind, add, gr);