Example overview

Autoregressive models take the general form:

$$ y_t = x_t \beta_t + u_t\\ u_t - \phi_1 u_{t-1} - \ldots - \phi_p u_{t-p} = e_t\\ e_t \sim N(\theta, \sigma^2) $$

The time series module provides a number of routines for performing pre-estimation data analysis, model parameter estimation, and post-estimation diagnosis of autoregressive time series.

Preliminary and Partial Autocorrelations

Suppose we have stationary univariate time series data but are uncertain about the order of the regressive relationship. You may wish to first use the sample autocorrelation function to help identify the general structure of the model. This can be achieved in GAUSS using the autocormt and autocovmt functions.

autocormt

The autocormt function computes the autocorrelations for each column of a matrix. It assumes that all data has been demeaned and produces an output matrix containing the autocorrelations for each column of an input matrix.

autocormt requires three input arguments:

- X

- An N x K data matrix.

- f

- A scalar denoting the first autocorrelation to be computed

- l

- A scalar denoting the last autocorrelation to be computed.

Consider a time series that follows the purely autoregressive data generation process given by:

$$ y_t = 1.5 + u_t\\ u_t - 0.5u_{t-1} + 0.8u_{t-2} = e_t\\ e_t \sim N(0,1) $$

Realizations of any ARMA data generation process can be randomly created using the function simarmamt:

// Load TSMT library

library tsmt;

// Specify ARMA Parameters

b_sim = { 0.5, -0.8 };

// Specify MA order

q_sim = 0;

// Specify AR order

p_sim = 2;

// Specify deterministic features (constant and trend)

const_sim = 1.5;

tr_sim = 0;

// Number of observations

n_sim = 200;

// Number of series to simulate

k_sim = 4;

// Standard deviation of the error terms

std_sim = 1;

// Set seed for repeatable simulations

seed_sim = 5012;

// Perform simulation

y_sim = simarmamt(b_sim,p_sim,q_sim,const_sim,tr_sim,n_sim,k_sim,std_sim,seed_sim);

/*

** Visualize data

*/

x_plot = seqa(1,1,rows(y_sim));

// Draw graph

plotXY(x_plot, y_sim[.,1]);The code above will produce a 200X4 matrix of data that follows the AR(2) data generating process specified. Each column of the matrix represents a different random realization of the process. The code graphs the first realization (the first column of y_sim):

{kind=link}

Though the data generating process of the data above is known, it is generally more realistic that one will wish to estimate the parameters of an unknown data generating process behind a realization of data. To begin, consider finding the ACF and the PACF using the GAUSS autocor and pacf functions:

/*

** Find autocorrelations for 0 to 10 lags

*/

// Create 'y' by demeaning each column of 'y_sim'

y = y_sim - meanc(y_sim)';

// Find autocorrelations

first = 0;

last = 10;

a = autocor(y_sim, first, last);

// Display autocorrelations

a_lab = seqa(0,1,rows(a));

print "Lags"$~"ACF";

print ntos(a_lab~a, 4);This code calculates and lists the sample autocorrelations for lags 0 through 10 for each sample of data. All columns of the list have a precision of two decimal points. Column labels “Lags” and “ACF” are included at the top of the list. This list will change depending on the data that has been randomly generated but should look similar to:

Lags ACF 0 1 1 1 1 1 0.511 0.589 0.598 0.556 2 -0.158 0.0363 0.0987 0.0105 3 -0.0824 0.0527 0.152 0.135 4 0.524 0.501 0.571 0.588 5 0.745 0.751 0.741 0.685 6 0.343 0.545 0.497 0.373 7 -0.0297 0.223 0.229 0.175 8 0.139 0.171 0.276 0.363 9 0.53 0.39 0.485 0.552 10 0.559 0.579 0.587 0.456

As an alternative, a bar graph visually presents the autocorrelation information. For example,

/*

** Display Correlogram

*/

// Declare 'myPlot' to be a plotControl structure

// and fill with default values for bar plots

struct plotControl myPlot;

myPlot = plotGetDefaults("bar");

// Add a title

plotSetTitle(&myPlot, "Correlogram");

// Add axes labels

plotSetYLabel(&myPlot, "ACF");

plotSetXLabel(&myPlot, "Lag");

// Draw graph

x_lag = seqa(0, 1, 11);

plotBar(myPlot, x_lag, a[1:rows(a),1]);This produces the following output:

The pacf function supplements the diagnostic information in the ACF and finds the partial autocorrelation function. The previous example is easily extended to find the PACF for the same randomly generated data. The pacf function requires three inputs:

- x

- An N x 1 data vector.

- k

- A scalar denoting the maximum number of partial autocorrelation to compute.

- d

- A scalar denoting the order of differencing.

Note that in GAUSS the pacf function always begins with the minimum of one lag. Hence, if k=10, pacf will find the partial autocorrelations for lags 1 through 10. For example,

// Find PACF

b = pacf(y[1:rows(y),1], 10, 0);

// Display partial autocorrelations

b_lab = seqa(0, 1, rows(b));

print "";

print "Lags"$~"PACF";

print ntos(b_lab~b, 2);

/*

** Plot PACF

*/

// Declare 'myPlot' to be a plotControl structure

// and fill with default values for bar plots

struct plotControl myPlot;

myPlot = plotGetDefaults("bar");

// Add a title

plotSetTitle(&myPlot, "Partial Autocorrelation Function");

// Add axis labels

plotSetYLabel(&myPlot, "PACF");

plotSetXLabel(&myPlot, "Lag");

// Plot PACF

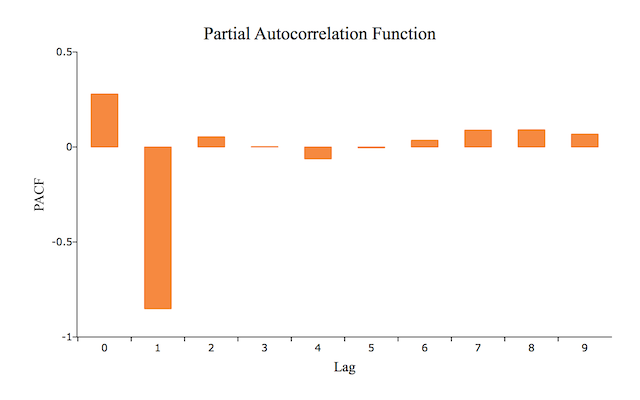

plotBar(myPlot, b_lab,b);This code calculates, lists, and graphs the partial autocorrelations for lags 0 through 10. This list and graph will change depending on the data that has been randomly generated but should look similar to:

Lags PACF

0 0.28

1 -0.85

2 0.054

3 0.0018

4 -0.062

5 -0.004

6 0.035

7 0.089

8 0.091

9 0.068

Estimating the Autoregressive Model

The arimamt function is a convenient tool for estimating the parameters of any ARIMA model, including ARMA models, purely AR models, and purely MA models. The arimamt function takes two arguments:

- ctl

- An

arimamtcontrol structure. - y

- N x 1 data vector

Note that this function can only be used to estimate models with a specified number of sequentially ordered lags. For example, it will estimate the parameters for the first through fourth lag but will not estimate a model that includes ONLY the first and fourth lag. In addition, note that this arimamt will produce an error if the data is not stationary and invertible.

The arimamt Control Structure

This structure handles the matrices and strings that control the estimation process such as specifying whether to include a constant, output appearance and estimation parameters.

Continuing with the example above,

// Declare 'ctl' to be an arimamtControl structure

// and fill with default values

struct arimamtControl ctl;

ctl = arimamtControlCreate();

// Declare 'out' to be an arimamtOut structure,

// to hold the results from 'arimamt'

struct arimamtOut out;

// Specify the AR order to 2

ctl.ar = 2;

// Specify order of differencing

ctl.diff = 0;

// Specify MA order

ctl.ma = 0;

// Include constant in model (default)

ctl.const = 1;This appropriately passes to arimamt that the model is an AR(2) model and includes a constant. The remaining control elements (the ones that we did not set above), left at the default values, specify preferences for output display and estimation.

With the control structure options set, we can now perform the estimation:

// Perform estimation with 'arimamt'

out = arimamt(ctl, y_sim[.,1]);which will return output similar to:

Model: ARIMA(2,0,0) Final Results: Log Likelihood: 718.584998 Number of Residuals: 200

AIC : -1433.169996 Error Variance : 1.056229913

SBC : -1426.573361 Standard Error : 1.027730467

DF: 198 SSE: 209.133522700

Coefficients Std. Err. T-Ratio Approx. Prob. AR[1,1] 0.51943 0.03673 14.14024 0.00000

AR[2,1]-0.85411 0.03654 -23.37306 0.00000

Constant: 1.89661768 Total Computation Time: 0.13 (seconds) AR Roots and Moduli: Real : 0.30407 0.30407 Imag.: 1.03843 -1.03843 Mod. : 1.08204 1.08204

Forecasting

We will produce forecasts from our model, using tsforecastmt. It takes five inputs:

- ctl

- An arimamtControl structure which, as we saw above, contains the AR and MA order of the model.

- b

- A vector of parameter estimates, possibly returned by

arimamt. - y

- A time series vector from which to produce forecasts.

- e

- A vector of errors, possibly returned from

arimamt. - h

- A scalar, the number of periods to forecast.

tsforecastmt returns a matrix with three columns, containing the lower forecast bound, the forecast and the upper forecast bound. Continuing on with our example, we will produce a 10 period forecast:

//Produce 10 period forecast

f = tsforecastmt(amc, amo.b, y_sim[.,1], amo.e, 10);will return output similar to:

Forecasts for ARIMA(2,0,0) Model. 95% Confidence Interval Computed. Period LCL Forecasts UCL Forecast Std. Err. 201 0.104811 2.124232 4.143652 1.030336 202 -0.461607 1.813988 4.089582 1.161039 203 -0.904040 1.659289 4.222618 1.307845 204 -1.130503 1.843919 4.818340 1.517590 205 -0.910903 2.071950 5.054802 1.521891 206 -1.264531 2.032700 5.329932 1.682292 207 -1.523356 1.817549 5.158454 1.704575 208 -1.726063 1.739318 5.204698 1.768084 209 -1.707635 1.882446 5.472526 1.831707 210 -1.578898 2.023608 5.626114 1.838047

The Command File

Finally we put it all together in the command file below, which will reproduce all output shown above.

// Load TSMT library

library tsmt;

/*

** Step 1: Simulate

*/

// Specify ARMA Parameters

b_sim = { 0.5, -0.8 };

// Specify MA order

q_sim = 0;

// Specify AR order

p_sim = 2;

// Specify deterministic features (constant and trend)

const_sim = 1.5;

tr_sim = 0;

// Number of observations

n_sim = 200;

// Number of series to simulate

k_sim = 4;

// Standard deviation of the error terms

std_sim=1;

// Set seed for repeatable simulations

seed_sim = 5012;

// Perform simulation

y_sim = simarmamt(b_sim,p_sim,q_sim,const_sim,tr_sim,n_sim,k_sim,std_sim,seed_sim);

// Visualize data

obs_num = seqa(1,1,rows(y_sim));

// Declare 'myPlot' to be a plotControl structure

// and fill with default values for xy plots

struct plotControl myPlot;

myPlot = plotGetDefaults("xy");

// Add a title

plotSetTitle(&myPlot, "AR(2) Data Simulation", "Times", 18);

// Set X and Y Axis labels

plotSetXLabel(&myPlot, "Observation");

plotSetYLabel(&myPlot, "Y");

// Plot 'y' observations

plotXY(myPlot, obs_num, y_sim[.,1]);

/*

** Step 2: ACF and PACF

*/

// Create 'y' by demeaning each column of 'y_sim'

y = y_sim - meanc(y_sim)';

// Find autocorrelations

first = 0;

last = 10;

a = autocor(y_sim, first, last);

// Display autocorrelations

a_lab = seqa(0,1,rows(a));

print "Lags"$~"ACF";

print ntos(a_lab~a, 4);

// Fill 'myPlot' with default values for bar plots

myPlot = plotGetDefaults("bar");

// Open new graphics tab so that we do not

// draw over our previous graph

plotOpenWindow();

// Add a title

plotSetTitle(&myPlot, "Correlogram", "Times", 18);

// Add axes labels

plotSetYLabel(&myPlot, "ACF");

plotSetXLabel(&myPlot, "Lag");

// Plot ACF

x_lag = seqa(0, 1, 11);

plotBar(myPlot, x_lag, a[1:rows(a),1]);

// Find PACF

b = pacf(y[1:rows(y),1], 10, 0);

// Display partial autocorrelations

b_lab = seqa(0, 1, rows(b));

print "";

print "Lags"$~"PACF";

print ntos(b_lab~b, 2);

// Add a title

plotSetTitle(&myPlot, "Partial Autocorrelation Function");

// Add axis labels

plotSetYLabel(&myPlot, "PACF");

plotSetXLabel(&myPlot, "Lag");

// Open new graphics tab so that we do not

// draw over our previous graph

plotOpenWindow();

// Plot PACF

plotBar(myPlot, b_lab,b);

/*

** Step 3: Estimate

*/

// Declare 'amc' to be an arimamtControl structure

// and fill with default values

struct arimamtControl amc;

amc = arimamtControlCreate();

// Declare 'amo' to be an arimamtOut structure,

// to hold the results from 'arimamt'

struct arimamtOut amo;

// Specify the AR order to 2

amc.ar = 2;

// Specify order of differencing

amc.diff = 0;

// Specify MA order

amc.ma = 0;

// Include constant in model (default)

amc.const = 1;

// Perform estimation with 'arimamt'

amo = arimamt(amc, y_sim[.,1]);

/*

** Step 4: Forecast

*/

/ /Produce 10 period forecast

f = tsforecastmt(amc, amo.b, y_sim[.,1], amo.e, 10);