Goals

This tutorial builds on the previous Linear Regression and Generating Residuals tutorials. It is suggested that you complete those tutorials prior to starting this one.

This tutorial demonstrates how to test the OLS assumption of homoscedasticity. After completing this tutorial, you should be able to :

- Plot the squared residuals against predicted y-values.

- Run the Breusch-Pagan test for linear heteroscedasticity.

- Perform White's IM test for heteroscedasticity.

Introduction

In this tutorial, we examine the residuals for heteroscedasticity. If the OLS model is well-fitted there should be no observable pattern in the residuals. The residuals should show no perceivable relationship to the fitted values, the independent variables, or each other. A visual examination of the residuals plotted against the fitted values is a good starting point for testing for homoscedasticity. However, it should be accompanied by statistical tests.

Plot residuals versus fitted values

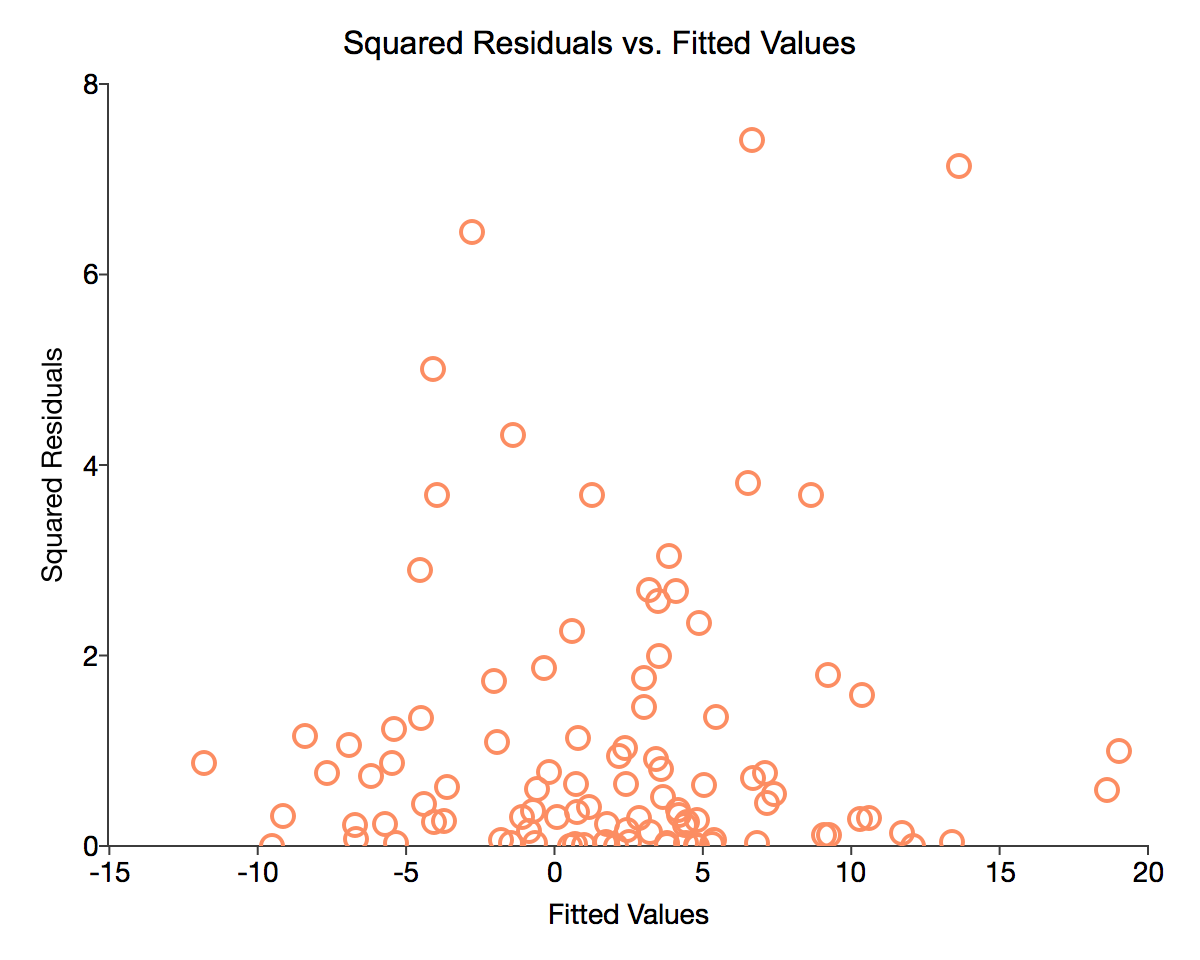

Our first diagnostic test will be to visually examine a chart of the residuals versus predicted y-values. As demonstrated in the previous tutorial, we have stored the residuals computed by the ols function in the variable resid. Using these residuals we compute the predicted y

$$\hat{Y} = X\hat{\beta}$$

// Add ones to x for constant

x_full = ones(num_obs, 1)~x;

// Predicted y values

y_hat = x_full*b;Charting the residuals versus the fitted y values allows us to look for any visual patterns of relationships between the fitted values and the error terms.

/*

** Plot histogram of residuals

** Set format of graph

** Declare plotControl structure

*/

struct plotControl myPlot;

// Fill 'myPlot' with default scatter settings

myplot = plotGetDefaults("scatter");

// Add title to graph

plotSetTitle(&myPlot, "Squared Residuals vs. Fitted Values", "Arial", 16);

plotSetXLabel(&myPlot, "Fitted Values");

plotSetYLabel(&myPlot, "Squared Residuals");

// Create scatter plot

plotScatter(myPlot, y_hat, resid.*resid);The code above should produce a graph similar to the image below:

Breusch-Pagan Test

The Breusch-Pagan test for heteroscedasticity is built on the augmented regression

$$ \frac{\hat{e}_i^2}{\hat{s}_i^2}\ = \alpha + z_it + \nu_i $$

where $ e_i $ is a predicted error term resid, $ s_i^2 $ is the estimated residual variance and $ z_i $ can be any group of independent variables, though we will use the predicted y values from our original regression. To conduct the Breusch-Pagan tests we will:

- Square and rescale the residuals from our initial regression.

- Regress the rescaled, squared residuals against the predicted y values from our original regression.

- Compute the test statistic.

- Find the critical values from the chi-squared distribution with one degree of freedom.

1. Square and rescale the residual from the original regression

Before running the test regression we must construct the dependent variable by rescaling the squared residuals from our original regression. The rescaling is done by dividing the squared residual by the average of the squared residuals. The result, a variable with a mean of 1, will become the dependent variable in our test regression.

/*

** Square the residuals

** The .* operator provides element-by-element multiplication

*/

sq_resid = resid .* resid;

// Find average of squared residuals

average_ssr = meanc(sq_resid);

// Rescale squared error

rescaled_sq_resid = sq_resid / average_ssr;2. Run the augmented regression

In order to construct the test statistic, we must run the augmented regression

$$\frac{\hat{e}_i^2}{\hat{s}_i^2}\ = \alpha + z_it + \nu_i $$

where $ e_i $ is a predicted error term, $ s_i^2 $ is the estimated residual variance and $ z_i $ can be any group of independent variables, though we will use the predicted y values from our original regression.

// Dependent variable in augmented regression

bp_y = rescaled_sq_resid;

// Independent variable in augmented regression

bp_z = y_hat;

// Run ols

{ bp_nam, bp_m, bp_b, bp_stb, bp_vc, bp_std,

bp_sig, bp_cx, bp_rsq, bp_resid, bp_dbw } = ols("", bp_y, bp_z);The code above should produce the following output report:

Valid cases: 100 Dependent variable: Y

Missing cases: 0 Deletion method: None

Total SS: 197.036 Degrees of freedom: 98

R-squared: 0.003 Rbar-squared: -0.008

Residual SS: 196.508 Std error of est: 1.416

F(1,98): 0.263 Probability of F: 0.609

Durbin-Watson: 2.149

Standard Prob Standardized Cor with

Variable Estimate Error t-value >|t| Estimate Dep Var

-----------------------------------------------------------------------------

CONSTANT 0.97528 0.149584 6.519966 0.000 --- ---

X1 0.01250 0.024379 6.519966 0.609 0.051733 0.051733

3. Construct test statistic

The Breusch-Pagan test statistic is equal to the augmented model sum of squares divided by two.

// Find predicted y

bp_y_hat = x_full*bp_b;

// Find regression sum of squares

bp_tmp = (bp_y_hat - meanc(bp_y));

bp_rss = bp_tmp'*bp_tmp;4. Find the test statistic critical values

The Breusch-Pagan statistic is distributed Chi-square (1). In general, high values of the test statistic imply homoscedasticity and indicate that the ols standard errors are potentially biased. Conversely, low values provide support for the alternative hypothesis of heteroscedasticity. More specifically, we should use the built in GAUSS function cdfChic can be used to find the p-value of the test statistic. cdfChic takes the following inputs:

- x

- Matrix, abscissae values for chi-squared distribution

- n

- Matrix, degrees of freedom.

// Calculate test statistic

bp_test = bp_rss/2;

print "Chi Square(1) =" bp_test;

// Calculate p-value

prob = cdfChic(bp_test, cols(y_hat));

print "Prob > chi2 = " prob;The above code should print the following output:

Chi Square(1) = 0.034952371 Prob > chi2 = 0.85169550

Our chi-square test statistic is very small and the p-value for our test statistic is 85.2%, exceeding 5%. This indicates that we cannot reject the null hypothesis of homoscedasticity.

White's IM Test

White's IM test offers an alternative test for homoscedasticity based on the r-squared from the augmented regression

$$ e_i^2 = \alpha + x_1 + x_2 + ... + x_i + x_1^2 + x_2^2 + ... +x_i^2 + x_1x_2 + x_2x_3 + ... + x_ix_j + \nu_i $$

The test statistic of $ N * R^2 $ tests the null hypothesis of homoscedasticity and has a chi-square distribution with $ \frac{K*(K+3)}{2}\ $ degrees of freedom.

1. Construct matrix of independent variables

Since we created the squared residuals for the previous test, we just need to construct the RHS variables for our augmented regression. In this case, we have only one independent variable in our original regression and our augmented regression equation is

$$ e_i^2 = \alpha + x_1 + x_1^2 + \nu_i $$

/*

** Construct independent variables matrix

** The tilde operator '~' provides horizontal

** concatenation of matrices

*/

im_z = x ~ x.^2;2. Run the augmented regression

We can use our newly created matrix im_z

// Dependent variable in augmented regression

im_y = sq_resid;

// Run ols

{ im_nam, im_m, im_b, im_stb, im_vc, im_std,

im_sig, im_cx, im_rsq, im_resid, im_dbw } = ols("",im_y,im_z);The above code will print the following report:

Valid cases: 100 Dependent variable: Y

Missing cases: 0 Deletion method: None

Total SS: 226.453 Degrees of freedom: 97

R-squared: 0.003 Rbar-squared: -0.018

Residual SS: 225.807 Std error of est: 1.526

F(2,97): 0.139 Probability of F: 0.871

Durbin-Watson: 2.148

Standard Prob Standardized Cor with

Variable Estimate Error t-value >|t| Estimate Dep Var

-----------------------------------------------------------------------------

CONSTANT 1.05013 0.18120 5.79548 0.000 --- ---

X1 0.07032 0.15796 0.44520 0.657 0.047440 0.051733

X2 0.01277 0.09751 0.13093 0.896 0.013951 0.028548

3. Construct test statistic

The final step is to find the test statistics $ N*R^2 $. This statistic is distributed Chi-square with $ \frac{K*(K+3)}{2}\ $ degrees of freedom. We again use the function cdfChic to find the p-value of the test statistic.

// Calculate test statistic

im_test = num_obs*im_rsq;

print "IM test" im_test;

// Find degrees of freedom

K = (cols(im_z));

im_dof = (K*(K+3))/2;

print "Degrees of freedom:" im_dof;

// Calculate p-value

prob = cdfChic(im_test, im_dof);

print "Prob > chi2 = " prob;The above code should print the following output:

IM test 0.28524914 Degrees of freedom: 5.0000000 Prob > chi2 = 0.99791134

The White IM test is consistent with the findings from our Breusch-Pagan test. Our chi-square test statistic is again very small and the p-value is greater than 5%. This means we cannot reject the null hypothesis of homoscedasticity.

Conclusion

Congratulations! You have:

- Plotted the squared residuals against predicted y-values.

- Computed the Breusch-Pagan test for linear heteroscedasticity.

- Computed White's IM test for heteroscedasticity.

The next tutorial examines methods for testing for influential data.

For convenience, the full program text is below.

// Clear the work space

new;

// Set seed to replicate results

rndseed 23423;

// Number of observations

num_obs = 100;

// Generate independent variables

x = rndn(num_obs, 1);

// Generate error terms

error_term = rndn(num_obs,1);

// Generate y from x and errorTerm

y = 1.3 + 5.7*x + error_term;

// Turn on residuals computation

_olsres = 1;

// Estimate model and store results in variables

screen off;

{ nam, m, b, stb, vc, std, sig, cx, rsq, resid, dbw } = ols("", y, x);

screen on;

print "Parameter Estimates:";

print b';

/**************************************************************************************************/

// Add ones to x for constant

x_full = ones(num_obs, 1)~x;

// Predicted y values

y_hat = x_full*b;

/*

** Plot histogram of residuals

** Set format of graph

** Declare plotControl structure

*/

struct plotControl myPlot;

// Fill 'myPlot' with default scatter settings

myplot = plotGetDefaults("scatter");

// Add title to graph

plotSetTitle(&myPlot, "Squared Residuals vs. Fitted Values", "Arial", 16);

plotSetXLabel(&myPlot, "Fitted Values");

plotSetYLabel(&myPlot, "Squared Residuals");

// Create scatter plot

plotScatter(myPlot, y_hat, resid.*resid);

/**************************************************************************************************/

/*

** Square the residuals

** The .* operator provides element-by-element multiplication

*/

sq_resid = resid .* resid;

// Find average of squared residuals

average_ssr = meanc(resid'*resid);

// Rescale squared error

rescaled_sq_resid = sq_resid / average_ssr;

// Dependent variable in augmented regression

bp_y = rescaled_sq_resid;

// Independent variable in augmented regression

bp_z = y_hat;

// Run ols

{ bp_nam, bp_m, bp_b, bp_stb, bp_vc, bp_std,

bp_sig, bp_cx, bp_rsq, bp_resid, bp_dbw } = ols("", bp_y, bp_z);

// Find predicted y

bp_y_hat = x_full*bp_b;

// Find regression sum of squares

bp_tmp = (bp_y_hat - meanc(bp_y));

bp_rss = bp_tmp'*bp_tmp;

// Calculate test statistic

bp_test = bp_rss/2;

print "Chi Square(1) =" bp_test;

// Calculate p-value

prob = cdfChic(bp_test, cols(y_hat));

print "Prob > chi2 = " prob;

/**************************************************************************************************/

/*

** Construct independent variables matrix

** The tilde operator '~' provides horizontal

** concatenation of matrices

*/

im_z = x ~ x.^2;

// Dependent variable in augmented regression

im_y = sq_resid;

// Run ols

{ im_nam, im_m, im_b, im_stb, im_vc, im_std,

im_sig, im_cx, im_rsq, im_resid, im_dbw } = ols("", im_y, im_z);

// Calculate test statistic

im_test = num_obs*im_rsq;

print "IM test" im_test;

// Find degrees of freedom

K = (cols(im_z));

im_dof = (K*(K+3))/2;

print "Degrees of freedom:" im_dof;

// Calculate p-value

prob = cdfChic(im_test, im_dof);

print "Prob > chi2 = " prob;