Introduction

This example follows the empirical example found in Hansen (1996) and estimates a threshold model for quarterly GNP growth rates. The data file "gnp.dat" contains seasonable adjusted GNP for 1947 to 1990 and is transformed into annualized quarterly growth rates.

Load data

This example loads the data using the GAUSS function loadd. The function loadd utilizes the GAUSS formula string syntax and allows users to load and transform specific variables directly from the dataset.

new;

library tsmt;

/*

** Real GNP data

** Seasonally adjusted and transformed in annualized quarterly growth rates

** 1947-1990

*/

// Load 'real_gnp' variable and perform 'ln' transformation

dataset = getGAUSSHome() $+ "pkgs/tsmt/examples/gnp_4790.csv";

ln_gnp = loadd(dataset, "ln(real_gnp)");

y = (ln_gnp[2:rows(ln_gnp)] - ln_gnp[1:rows(ln_gnp)-1]) * 400;Set Up the Estimation

The tarControl structure is used to control the model characteristics. This includes the number of lags considered, which lags to omit from the test, the number of replications, and graph features:

// Declare the structure

struct tarControl t_ctl;

// Fill 't_ctl' with default settings

t_ctl = tarControlCreate();

// Maximum number of lags considered

t_ctl.p = 5;

// Lags to omit from the test

// Consider lags 1, 2 and 5

t_ctl.omit = { 3 4 };

// Number of replications for Monte Carlo

t_ctl.rep = 5000;

// Data start date and frequency

t_ctl.dstart = 1947;

t_ctl.freq = 4;Estimate the Model

All output from the tarTest function can be stored in a tarOut output structure.

// Declare 't_out' to be a tarOut structure

// to hold the estimation results

struct tarOut t_out;

// Perform estimation

t_out = tarTest(y, t_ctl);

Output

The printed output from tarTest reads

OLS Estimation of Null Linear Model

Variable Estimate S.E.

C 1.99225488 0.59341810

Y(t-1) 0.31753696 0.08929921

Y(t-2) 0.13197878 0.08801236

Y(t-5) -0.08696297 0.06763670

Residual Variance 15.9605

Searching over Threshold Variable: 1

Searching over Threshold Variable: 2

Searching over Threshold Variable: 3

Global Estimates

Threshold Variable Lag 2.0000

Threshold Estimate 0.0126

Error Variance 14.5484

Regime 1: Y(t-2) < 0.012572

Variable Estimate S.E.

C -3.21255539 2.12039565

Y(t-1) 0.51278104 0.24699822

Y(t-2) -0.92692272 0.30831951

Y(t-5) 0.38445656 0.24603002

Regime 1 Error Variance 23.5331

Regime 2: Y(t-2) > 0.012572

Variable Estimate S.E.

C 2.14186153 0.77389336

Y(t-1) 0.30085440 0.10132777

Y(t-2) 0.18484356 0.10131018

Y(t-5) -0.15813482 0.07335517

Regime 2 Error Variance 12.1430

Test Statistics and Estimated Asymptotic P-Values

Robust LM Statistics

SupLM 14.06847762 0.17300000

ExpLM 3.96481133 0.16720000

AveLM 4.68986250 0.29240000

Standard LM Statistics

SupLMs 18.24477743 0.94920000

ExpLMs 4.77627149 0.94760000

AveLMs 4.57209118 0.88940000

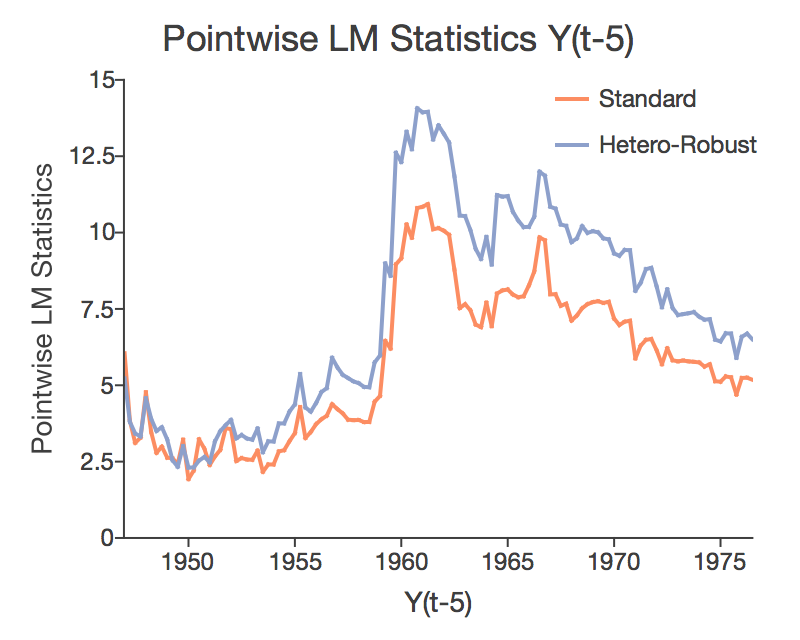

In addition, the procedure produces the graph at the top of this page and the two below.